fjrigjwwe9r3SDArtiMast:ArtiCont

medication abortion

order abortion pill online

|

New pension regime in focus

The annuity buying process gains significance in the light of new guidelines by the Insurance Regulatory and Development Authority ( Irda) on pension plans, which have heralded several changes. Under the new regime, policyholders will not have the choice of approaching the insurer which offers the best annuity rates at the time of vesting. This has been done to reduce the burden on PSU behemoth LIC, which rules the space currently. This makes it imperative for the investors to choose wisely while buying a pension plan as they will need to factor in the insurer’s capabilities. "While buying a pension plan, it’s important that you evaluate the insurer thoroughly. In addition to this, you should track how the corpus has been managed over the past few years, the charges and fees, the convenience of transaction and payout history," says Vishal Kapoor, head of wealth management, Standard Chartered Bank.

|

While rates are important, you should not base your decision solely on the ones being offered currently. "The annuity rate at the time of buying a pension plan need not be an indicator of what you would get when you need to buy annuities in future," cautions Sanjeev Pujari, appointed actuary, SBI Life. So far, nearly 21 products have been filed with the insurance regulator for approval since the new norms became effective from 1 January this year. Recently, MetLife launched a deferred annuity, or pension, plan and SBI Life announced an immediate annuity scheme.

|

Choosing the right annuity structure

Annuities refer to the stream of income an insurer pays at regular intervals until your death or the end of the tenure you may have opted for. The corpus at the end of the accumulation phase will be paid out in two parts -one-third as a lump sum and the balance being converted into annuities. You will need to buy annuities using the amount accumulated by your pension plan or any lump sum. The annuity option you choose will depend on your requirements and expectations from the plan. This will be applicable primarily to those investors who may have built the corpus through pension plans until January this year and others with a fund pool. |

As mentioned earlier, those buying pension plans henceforth will have to settle for the annuities offered by their insurer. Within the basket of annuity plans offered by your insurer, though, you still have to use your discretion. This will be applicable to everyone looking to buy annuities, irrespective of the date of purchase. "While zeroing in on the right option, you need to ponder upon three questions-what kind of income you would need, whether your annuity requirement would go up or remain the same throughout your lifetime and whether you would like to redirect the proceeds to your spouse upon your death," says Pujari. Adds Kapoor: "While buying annuities, customers should consider the expected rate of return (annuity rate) along with the charges, the period of annuity desired (whether for life or for a fixed period), flexibility in joint ownership and the payout."

Know your annuity

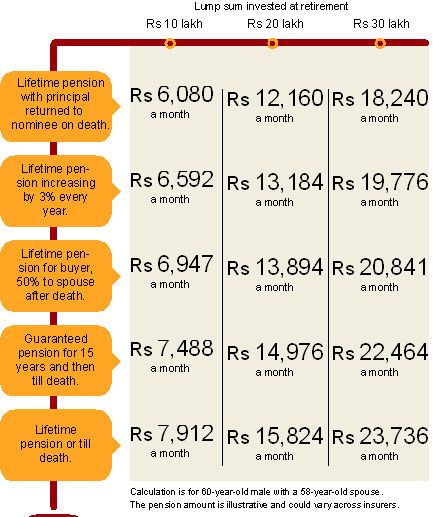

After you have evaluated your requirements, you can choose an annuity option that suits your needs best. Broadly, annuity plans are categorised into five segments (see The pension you can earn), though the range of options could vary depending on the insurer. The pension you can earn

Here’s a look at how much you will get each month depending on the investment.

|

Annuity payable for life

You will be paid a fixed annuity at regular intervals throughout your life. The insurer will stop paying pension after your demise. This is why annuities are suitable for those who do not have any obligation after death. This option offers the highest amount of pension for an individual compared to any other option available.

Annuity payable for life with a guaranteed period

Here, annuity is paid for a certain number of years, say, the chosen term of 10 years, and thereafter as long as the annuitant is alive. The shorter the guarantee period, the higher is the pension. The annuity stops upon either the death of the annuitant or completion of the guaranteed period, whichever is later. This is a simpler tool to ensure income for the family for a stipulated period of time. For example, you retire at a time when you are still the sole earning member in the family, but expect your children to start earning after five years. In such a case, you could consider an annuity that is guaranteed for five years. |

Life annuity with return of corpus

This option works for those who want to leave a legacy for their nominees. Here, the annuitant enjoys the pension till he dies. After his demise, the purchase price of the annuity (that is, the premium paid by the buyer of the annuity) is handed over to the nominee. This is a popular option as both the annuitant and the nominee stand to benefit. Some new variants also offer to return the purchase price in instalments.

Life annuity increasing at a fixed rate

Under this option, the annuity amount payable each year increases at a certain rate, say 3-5%. "While this rate is not linked to the actual inflation rate, the rationale is that the increased amount would take care of the rise in expenses to an extent," says Pujari.

Joint life and last survivor annuity

As the name denotes, the annuitant is entitled to receive the pension throughout his lifetime. If the spouse survives the annuitant, the former is also entitled for the pension, ensuring ’lifestyle maintenance’ of the spouse. The buyer can further choose the quantum of pension (50% or 100% of the annuity) payable to the spouse.

Annuity versus other investments

Though there are various advantages of investing in annuities, you should refrain from putting all your eggs in the annuity basket. "Income from annuities is taxable. Therefore, while buying one, you should ensure that your annual income from an annuity is within the no-tax limit," says Lovaii Navlakhi, managing director and chief financial planner, International Money Matters. You can also consider other tax efficient avenues such as short-term debt mutual funds or tax-free bonds. "Annuity income is fixed, and if the interest rates move up, you may not get to participate in it. This makes it important to ensure that your portfolio gets some exposure to instruments that are liquid," adds Navlakhi. In other words, you would be in a secure position if you have allocated your savings among a mix of products that complement each other.

|

So, to ensure that you continue to live comfortably in your sunset years, you need to invest wisely in the right type of annuity as well as put money in secure debt instruments. |

|

Industry News

Industry News